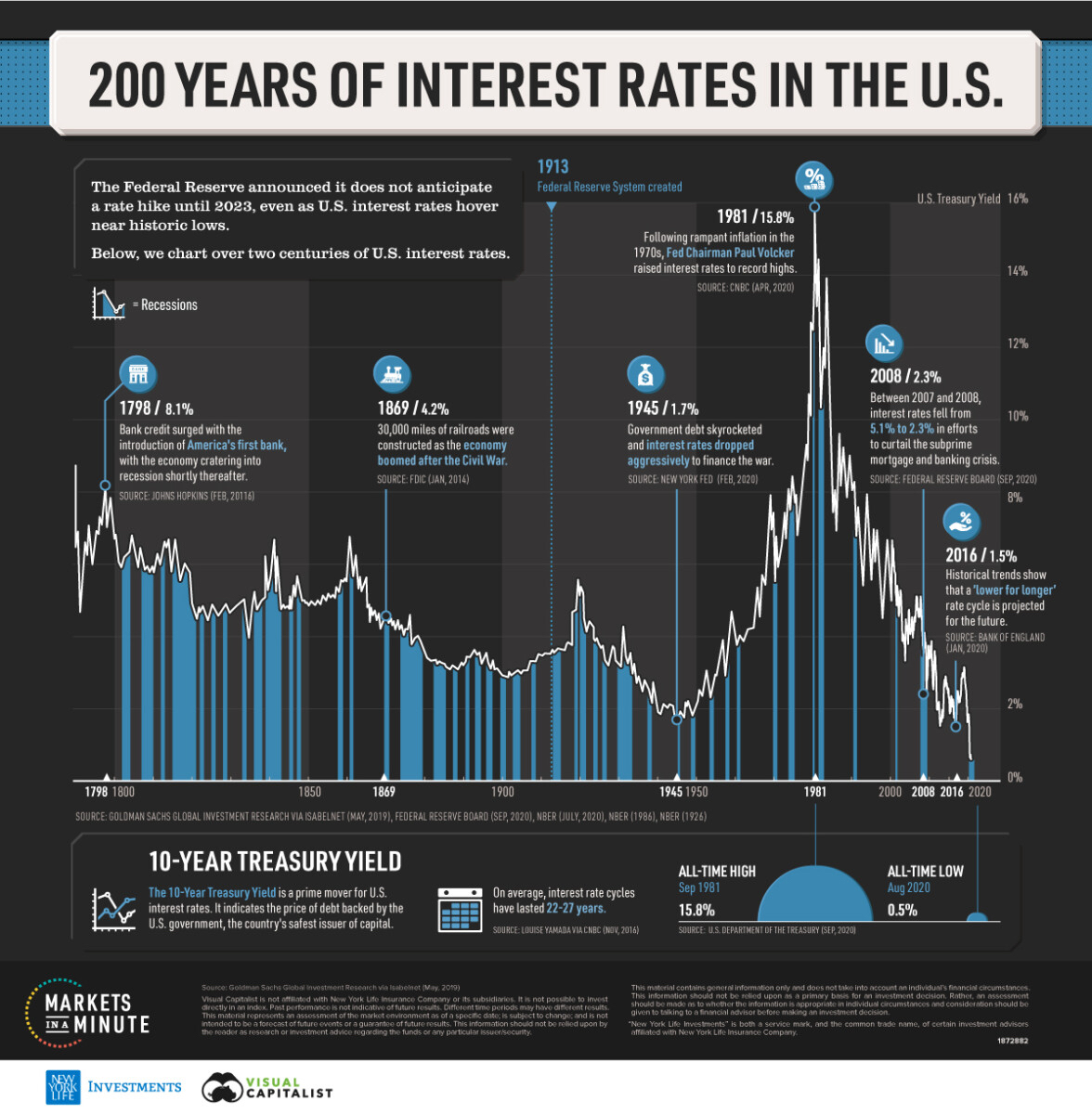

This summer, the yield on the 10-year treasury bond hit an all-time low of 0.50%. It’s easy to brush off that statistic but it is absolutely astounding once you see it in a historical context like the chart below.

The yield has come up a bit as of this writing (0.74% as of 10/16/20), but still paltry in the grand scheme of things. The 10-year treasury is an important benchmark as it helps to set things like mortgage rates and auto loans. For those of us borrowing money, this is obviously a great environment (just ask any mortgage broker how busy they’ve been this year). But for those of us that have some of our investments in bonds, this is going to be a challenging environment going forward to say the least. If the 10 year treasury offers a yield of less than 1%, and a diversified portfolio of bonds today offer yields of 2-3% if you’re lucky (a whopping 80% of all bonds are yielding under 1% globally) , then what should you do with your bonds now?

Your performance this year will not look the same in the future

If you look at the return on your bonds this year, you might not be that concerned. After all, the benchmark index for bonds (measured by the ETF symbol AGG), has returned 7.22% YTD as of 10/16/20. Over the last 10 years, the total return is 41.89%, or 3.56% per year. You could easily have put a portion of your portfolio in a fund like this and gotten a combination of income that outpaced inflation, diversification for your equity portfolio, and principal protection.

So what’s the problem? That return is virtually impossible to replicate going forward. Why?

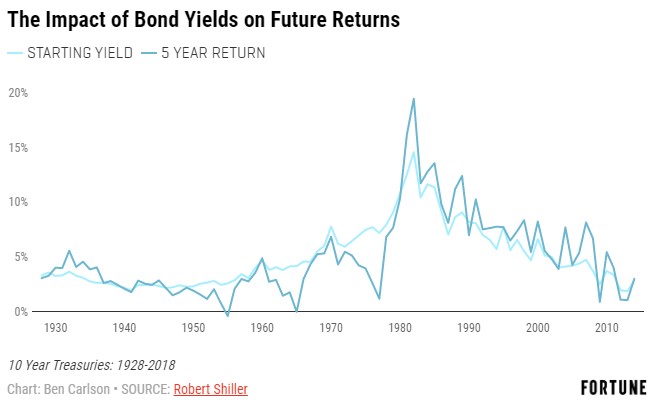

Most of the return on your bond funds can be measured by the starting yield

Source – Fortune

Using the chart above, you can see the correlation between the starting yield of your bond (measured here by the 10-year treasury) and your 5-year total return. You can see how correlated they are. It should make sense. Remember, bonds are just loans – loans to corporations, governments, etc.

In a simple example – let’s say you bought a Microsoft bond for $10,000 maturing in 2030 for a 4% coupon. Microsoft will pay you $400 / year for 10 years and at the end of the term will give you your $10,000 back. Easy. All you have to hope for is that Microsoft is around and solvent for the next 10 years to pay you your interest and principal back and you are all set. Your annual total return over 10 years is 4%.

Where it gets interesting is when you see your statement this year and see that the price of your Microsoft bond is up 8.11% (the approximate increase in price if interest rates fall by 1%). If we agree that your total return is measured almost completely by your starting yield, then where did the additional return come from? Price appreciation from falling interest rates.

Coupon + price appreciation = total return.

Let’s go back to the Microsoft example. In the interim of the 10 years you hold your bond, the price will fluctuate. This is due to a few factors, namely changes in current interest rates, changes in the creditworthiness of the issuer, and overall demand for bonds in general. Using the prior example, you may look at your statement 3 years into the term and see that your $10,000 bond might be worth $11,000 in the open market. It may only fetch $9,000. But in reality, as long as you hold your bond until maturity, you’ll get your $10,000 back and the price fluctuation is a moot point.

But in years that you see the price of your bond has gone up like this year, you may be happy. In reality, all you are seeing is future returns pulled forward. If you know the total return of your bond is 4%, and it’s worth more than that today, it means your future returns will be less.

Now most of us don’t own individual bonds, we use bond funds like AGG mentioned in the top of this post. AGG owns a diversified portfolio of government, agency, and corporate bonds. Yes, the 7.22% YTD return is great. What isn’t is the 1.22% yield that it offers now. If we know our starting yield dictates the majority of our future returns, it’s not hard to see why bonds will not return nearly as much as they have in the recent past. And we haven’t even talked about what happens to the bond math when interest rates finally start to go up and the price appreciation turns into price depreciation.

So what should you do now?

Accept lower returns in your bond portfolio and stick with it

You may not want to take any additional risk, which is fine. If your financial plan still works with assuming reduced returns in your bonds going forward, there is no reason you can’t stick with what you have. As you are aware, chasing higher returns can have consequences. What you can lose in a year in bonds you can lose in a day in stocks.

Someday interest rates will go up again and, while that usually involves a reduction in the price of your bond portfolio, this is ultimately a good thing as your bond income will eventually go up as well.

Prioritize income or equity diversification

Make sure your bond mix is focused on the right priority. Depending on your goal, focus on either income or equity diversification as it’s going to be hard to get both going forward.

Are you a younger or more aggressive investor with 10-20% of your portfolio allocated to bonds? Bonds still serve a purpose, but income probably isn’t one of them. Especially when you can sell them to rebalance back into stocks in times like March of 2020. I’d argue that equity diversification is more important for you and things like US government bonds and high-quality corporate bonds still have a place. When the S&P 500 tumbled in March, US Treasury bonds performed well. For now, quality bonds are still acting like a good hedge against your equity portfolio.

Are you more conservative and have most of your money in bonds? I’d argue that income is probably more important than equity diversification. In your case, I’d be looking to add things like high yield, emerging market, or non-US agency mortgage bonds that offer higher yields. Like mentioned above, these asset classes offer higher returns for a reason so do your homework before adding them.

Is principal protection the most important thing for you? That’s fine – just know that you’ll be losing money each year due to inflation. This is going to be a very tough environment to earn a return over inflation without taking some kind of risk with your portfolio.

Think of alternatives

There are other asset classes out there you may want to consider as an alternative to a portion of your bond sleeve. Real estate, preferred stocks, and dividend paying stocks can all offer some combination of increased income and capital appreciation potential. Some investors are carving out a piece of their bond portfolio to buy gold to protect themselves against future inflation (I wrote about investing in gold here). You may also want to look at paying down your mortgage or other debt. After all, this is a guaranteed rate of return and probably one that is more than what you’re getting in your bonds now. I’ll be going more in depth into income-producing alternatives in a future post.

Bond investors will be challenged to make the same returns as they’ve been used to. Plan accordingly.